Learn more about Colin Shaw: Join over 80,000 people on our LinkedIn Newsletter list or visit our website for more great podcast episodes.

Listen to the podcast:

I am excited. My wife and I are going on a cruise to India. It’s a big splurge for us, and we look forward to it. I mention it here, not to rub it in your face (much), but because in the booking of this cruise, I saw an excellent example of how my wife and I leverage mental accounting regarding our splurges.

When my mother-in-law passed, she left money for my wife, Lorraine. After I booked it, she commented that the inheritance paid for the cruise. As she said it, I thought, “Sure…but with that booking, we have now spent that money 27 times.”

We haven’t, of course, but the idea here was that we mentally allocated that money toward the cruise and had done so with that money numerous times. It was our version of Mental Accounting.

People have various rules regarding found money. For example, we spend unexpected bonuses or investment payoffs differently than what we earn. We consider it an opportunity to spend it specially.

Mental Accounting is a Side Effect of Cognitive Biases

Money is fungible, which is a fancy $3 word for something that is infinitely transferable. It’s a way to explain how money in your bank account, no matter where it is from, can be used for anything. You could pay for dance lessons with it or your mortgage. Once you’ve got the money, it is there, and you can use it anywhere.

Mental Accounting ruins all that. Mental Accounting divides that money and earmarks it for certain purposes, taking away its fungibility in our heads.

What makes this interesting is that our Mental Accounts suffer from all the other biases of our cognitive processes. For example, we’re not good at keeping track of these things. We draw on that sum willy-nilly as we need to feel better about certain purchases.

In the case of Lorraine’s inheritance, we would feel better if the cruise amount came out of that mental account than what we have set aside for retirement. Plus, her mum would have wanted us to treat ourselves, so we feel better about spending the money she left Lorraine on something like this.

It reminds me of a podcast with Joe Pine regarding time well spent, time well saved, and time well invested. It denotes how we mentally put different values on those things and how we use time.

However, we do not treat time and money the same way; there are differences. We do mentally allocate time, though, and it affects behavior. In some extreme cases, people who have allocated their time to a task can hardly do anything else with it if there is an obstacle to completing or working on the task. The same goes for money; some people have such discipline with their spending via mental accounting that they have difficulties with flexibility there.

My Daughter Does it, Too.

So, Lorraine isn’t the only one with these mental accounting foibles. My daughter is guilty of it, too. She has a vacation account to which she commits regular contributions, too. (Vacations are important to the ShawsShaws, apparently.)

Recently, she needed a new washing machine. She acted like she couldn’t afford it. She had plenty of money in her vacation account to cover it, but she was appalled at taking any money for something as mundane as a washing machine. That money was for vacation, after all!

I understand her position here. A washing machine is an un-sexy purchase, and who wouldn’t want to spend that money on vacation?

However, in this example, my daughter has a mental allocation for the money and a physical account for vacation funds. Having a physical account is a tactic for staying on budget, mental or otherwise. As I mentioned, those mental accounts can be slippery, but a physical bank account is not.

However, physical money or goods affect our mental accounting, too. Kahneman and Tversky, the economist team whose work resonates throughout behavioral economics, had this early demonstration of mental accounting. They asked people to imagine that they wanted to go to a concert. They told one group they already bought a ticket; the other group had $20 cash in their pocket to buy it at the theatre. However, upon arrival at the concert, the participant lost the ticket or the cash. So, now, what would the participant do?

The results were surprising. Even though the participant was down $20 in both scenarios, those who lost the cash were more likely to buy another ticket. Purchasing a second physical ticket after already having one was too much for many people’s mental accounting.

Also, financing can create mental biases around spending physical accounts. For example, if the offer is zero percent financing, you might take that deal rather than pay upfront, even if you have the cash to pay outright. The mental accounting here is that you can do better than zero percent interest for the money you hang onto, so making payments is financially beneficial over parting with the lump sum. Then, even though you spent that money in the physical bank account and will give it to the company over time, you still have it in your account, so it doesn’t hurt as much.

The other side of that decision is that paying upfront instead of financing might make you enjoy the purchase less. The pain of parting with the physical money will impinge upon the pleasure you get from buying something you want.

Mental Accounting Helps Us Manage Emotions

What we can see from these examples is that mental accounting helps us manage our emotions regarding our spending. We can feel guilty about spending, even feel a twinge of “pain” by parting with our money. By mentally accounting for it, we separate the pain of spending from the enjoyment of purchasing.

Credit cards do that, too. You get the joy of purchase immediately and delay the pain of spending to a later date. That’s why credit cards can be financially dangerous for some of us; separating the pain of payment lifts our restraints on spending. Moreover, the aggregate expenditures of a month reduce the pain of any individual purchase.

So, What Should You Do With This Information?

From a Customer Experience perspective, mental accounting has some key strategy points. To begin with, what we buy could fit into multiple mental accounts. So, is there a way to frame the purchase to nudge the customer to think about the purchase in a way conducive to guilt- and pain-free spending?

For example, if the product you sell replaces windows or doors in someone’s home, can you frame the purchase as regular maintenance, which often has a mental account in homeowners’ minds? Or as an investment in or improvement for their asset? If so, customers might allocate that spend to a mental account that makes the price accessible for them and increases feelings of satisfaction about the purchase.

Also, payment methods have more or less pain of payment associated with them. Cash is the most painful way, followed by checks. Credit cards are not as painful as cash and checks. Ostensibly, payment methods like tapping cards or Smartphone purchases could be even less painful than credit cards. So, how can you use that in your transaction to help customers manage their emotions about spending?

If you can reframe the spending in a way that feels better for people, you can improve the spending experience.

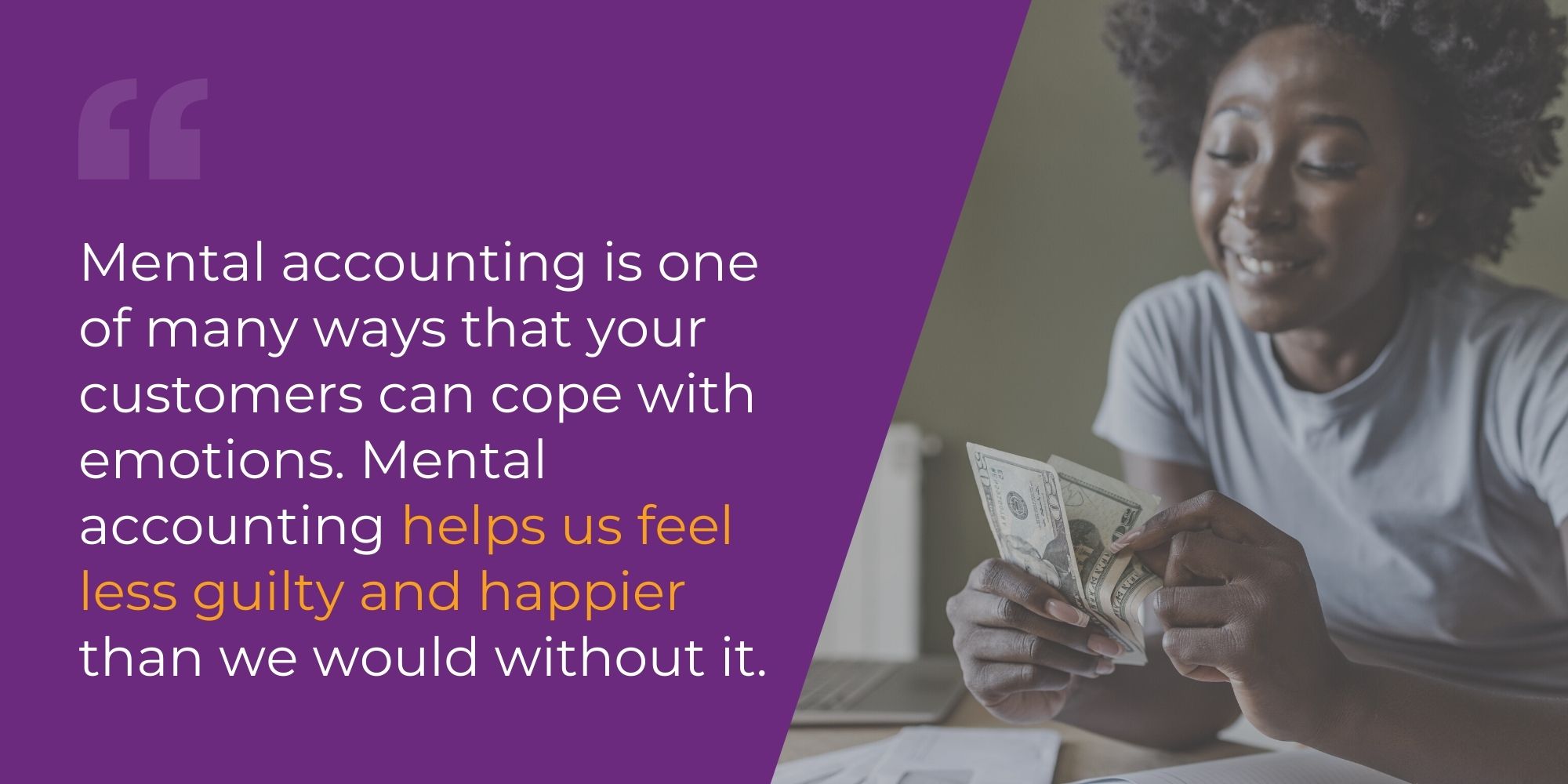

Mental accounting is one of many ways that your customers can cope with emotions. Mental accounting helps us feel less guilty and happier than we would without it. So, consider customers’ mental accounting within the broader context of managing your customers’ emotions.

Therefore, knowing where your customers are and, from your perspective, where you would like them to be can help you find the proper messaging supporting that.

Have something to say? We are looking for people to share their new ideas, opinions, thoughts, reports, or statistics in a 5-minute video & audio. We will run this at the show’s top, and Colin will discuss it with his co-host, Professor Ryan Hamilton. This is an excellent opportunity to get your message to a vast audience. Currently, the podcast has 12,000 downloads per month on average!

If you’re interested in submitting, fill out the form here.

Thanks for reading, we appreciate you! Get access to your free ebook here and why not tell a friend?